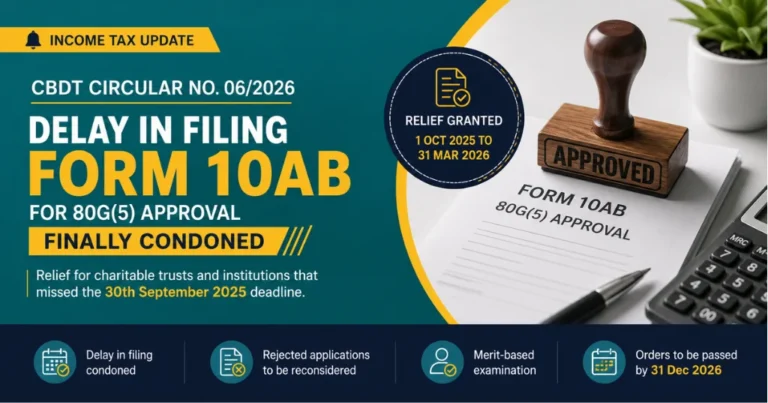

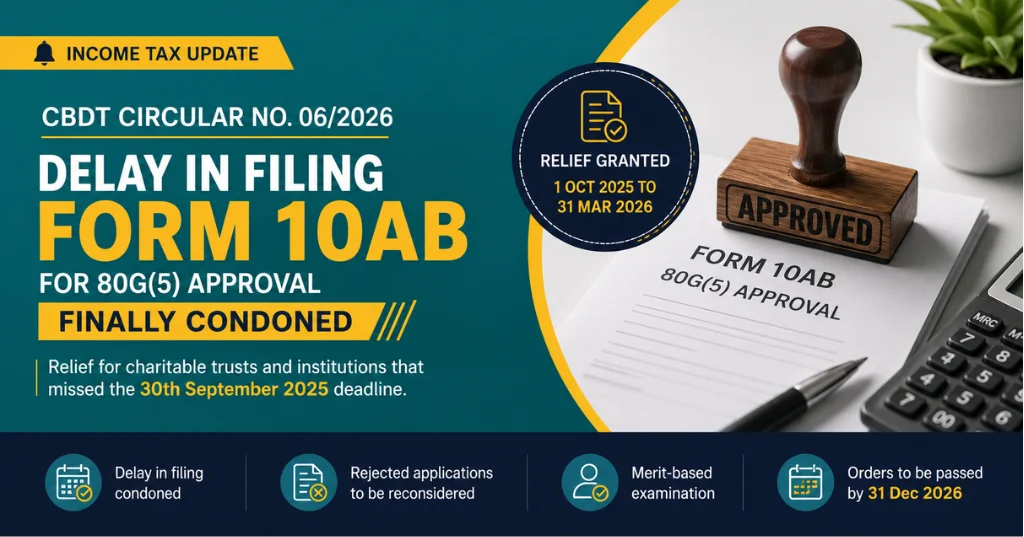

Income Tax Update • CBDT Circular

Relief for charitable trusts and institutions that missed the 30th September 2025 deadline — here's what actually happened, why it happened, and how you can get your 80G approval back on track.

01 A Quick Look Back: Why Form 10AB Exists

Section 80G of the Income-tax Act, 1961 allows donors to claim a deduction for donations made to approved charitable funds and institutions. But this approval isn't permanent — under the current registration regime, most 80G approvals are granted for a fixed period (commonly five years), after which the trust or institution must apply afresh for renewal. This renewal application is filed electronically in Form No. 10AB, and the law requires it to be submitted at least six months before the existing approval expires. For a large number of trusts, NGOs, and charitable institutions whose 80G approval was set to lapse on 31st March 2026, this meant the renewal application was due by 30th September 2025 — a deadline that came and went quietly for many organisations, setting the stage for the problem CBDT has now had to step in and fix.

02 The Problem: Missed Deadlines, Genuine Hardship

In the months following the 30th September 2025 due date, CBDT started receiving representations from charitable funds and institutions across the country who simply could not file Form 10AB in time. The reasons cited were largely procedural and administrative in nature — trusts unaware of the six-month advance filing requirement, confusion around the transition of provisions from the Income-tax Act, 1961 to the newly enacted Income Tax Act, 2025 (which now houses the corresponding provision under Section 133), portal or documentation issues, and general compliance fatigue that smaller institutions often face without dedicated tax teams.

The consequences of missing this deadline were serious. Without a valid, renewed 80G approval, an institution's donors would no longer be able to claim tax deduction benefits on their contributions — directly threatening the institution's ability to raise funds. Worse, several trusts that did manage to file Form 10AB late — between October 2025 and March 2026 — found their applications outright rejected by the tax department for the sole reason that they were filed beyond the 30th September 2025 cut-off, with no consideration given to the merits of the application itself. This left a large number of genuine charitable institutions staring at the loss of their 80G status purely on a technicality.

03 What CBDT Circular No. 06/2026 Actually Says

Recognising this as a case of genuine hardship, CBDT examined the matter and issued Circular No. 06/2026 dated 2nd July 2026 (F. No. 300176/3/2026-ITA-I), exercising its powers under Section 119(2)(b) of the Income-tax Act, 1961 read with Section 536(2) of the Income Tax Act, 2025. In plain terms, the circular does two specific things:

1. Delay Condoned for Fresh Filings

Where Form No. 10AB has been furnished electronically anytime between 1st October 2025 and 31st March 2026, the delay in filing stands condoned. The jurisdictional Principal Commissioner of Income-tax (PCIT) or Commissioner of Income-tax (CIT) is now authorised to examine such applications on merits and pass an order on or before 31st December 2026.

2. Relief for Applications Already Rejected

Where a Form 10AB application filed within this same window (1st October 2025 to 31st March 2026) was already rejected solely on the ground of being late, that rejection is now deemed condoned. Such cases too will be reopened and reconsidered by the jurisdictional PCIT/CIT on merits, with an order to be passed on or before 31st December 2026.

Importantly, the circular carries a clear caveat: condonation of delay is not the same as approval. It does not confer any automatic entitlement to approval under Section 80G(5) of the Income-tax Act, 1961, or the corresponding Section 133(1)(b) of the Income Tax Act, 2025. Every application will still be scrutinised independently on its own merits before a decision is taken.

04 How Institutions Actually Get Relief

Here is what this means in practical terms for a trust or institution affected by the delay:

- Already filed late (Oct 2025 – Mar 2026), application still pending: No fresh action is required for the delay itself — it stands condoned. The jurisdictional PCIT/CIT will now examine the application on merits and is expected to pass an order by 31st December 2026.

- Already filed late and already rejected only due to delay: The rejection is deemed condoned. Institutions should follow up with their jurisdictional PCIT/CIT to ensure the case is taken up afresh for a merit-based decision by the same deadline.

- Have not filed Form 10AB at all yet: This circular only condones delay for applications filed between 1st October 2025 and 31st March 2026 — it does not extend the window beyond 31st March 2026. Institutions in this position should seek professional advice immediately to understand their current status and available remedies.

Note: Condonation of delay is procedural relief only. The final approval still depends on the institution meeting all substantive conditions under Section 80G(5). Ensure your documentation, activities, and compliance history support your case before the order is passed.

Find Our Latest ITR, Registration & Compliance Pages

- ITR Filing for NRIs

- ITR Filing for Content Creators & Influencers

- ITR Filing for Event Management Professionals

- Income Tax Return Filing in Mumbai

- ITR Filing for Healthcare Industry