A very common question business owners, freelancers, and influencers ask is: “What is the maximum bank transaction limit before the Income Tax Department notices me?”

There are countless stories of individuals panicking because their bank accounts were suddenly frozen due to crossed thresholds. Many independent professionals operate under a dangerous myth: “I operate on a small scale; no one is watching my transaction limits.”

The reality is vastly different. The system no longer relies solely on what you voluntarily declare. Through forensic data aggregation and automated systemic reporting, the Income Tax Department tracks your financial footprint instantly. Let’s decode exactly how the government monitors your transactions, what the statutory limits are, and how you can safeguard your financial health.

The PAN Hub: Statement of Financial Transactions (SFT)

The government does not need you to maintain a perfect ledger to know your lifestyle. Through the Statement of Financial Transactions (SFT) under Section 285BA of the Income Tax Act, banks, registrars, and financial institutions are legally mandated to report specific high-value transactions directly to the IT Department.

Your PAN card acts as the central hub connecting these data points. If you cross the following factual thresholds in a single financial year, an automatic alert is generated in your Annual Information Statement (AIS):

- Cash Deposits & Withdrawals: Depositing ₹10 Lakhs or more in aggregate in savings accounts, or ₹50 Lakhs or more in current accounts.

- Credit Card Usage: Cash payments of ₹1 Lakh or more towards credit card bills, or payments of ₹10 Lakhs or more through any mode (NEFT/IMPS/Cheque) settling credit card dues.

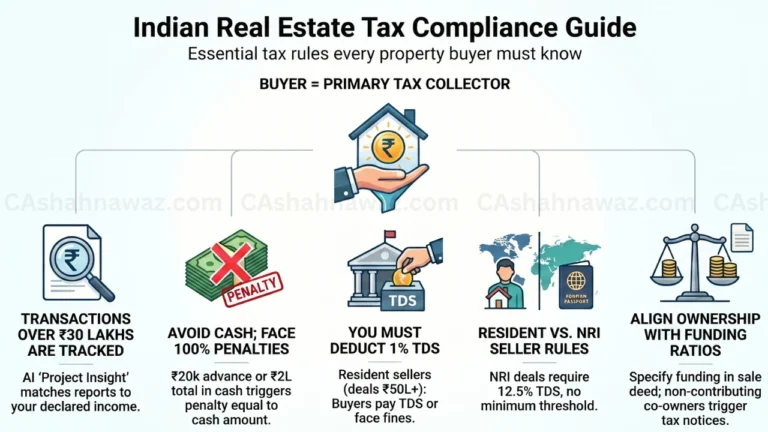

- Real Estate Transactions: Purchasing or selling immovable property valued at ₹30 Lakhs or more (reported by the Property Registrar).

- Investments (Shares, Bonds, Mutual Funds): Investing ₹10 Lakhs or more in shares, mutual funds, or acquiring bonds/debentures.

- Foreign Exchange & Travel: Purchasing foreign currency or spending on foreign travel exceeding ₹10 Lakhs.

GST Thresholds: Strict Rules Based on Business Type

When it comes to Goods and Services Tax (GST), liability depends entirely on your gross turnover, not your profit. GST registration becomes strictly mandatory the moment your total annual turnover crosses these exact limits:

- Goods & Trading (Buying and selling physical products): The threshold limit is ₹40 Lakhs in most states (including Maharashtra).

- Services & Hybrid Businesses (Restaurants, freelancers, software developers, influencers): The threshold limit is ₹20 Lakhs.

Crucial Caveat: If you make inter-state supplies (selling outside your home state) or operate through e-commerce operators (like Amazon, Zomato, or Upwork), GST registration is mandatory irrespective of your turnover limit.

Income Tax Targets Your Retained Profit

While GST focuses on your top-line revenue, Income Tax targets what you actually keep—your net profit.

- The Baseline Trigger: Under the new tax regime, the basic exemption limit is ₹3 Lakhs, but practically, with the Section 87A rebate, income up to ₹7 Lakhs can be tax-free. However, filing an Income Tax Return (ITR) becomes strictly mandatory if your gross total income exceeds the basic exemption limit (₹3 Lakhs under the new regime, ₹2.5 Lakhs under the old regime for individuals below 60).

- Scenario A: You earn ₹5 Lakhs net profit. Action: Income tax filing is mandatory, even if your tax liability ends up being zero due to rebates.

- Scenario B: You earn ₹15 Lakhs net profit. Action: You incur a significant tax liability according to the applicable slab rates, and filing is mandatory.

The Forensic Blueprint: Reverse-Engineering Hidden Wealth

What if someone keeps an “empty ledger” and intentionally maintains no official business records? The government uses a forensic blueprint to reverse-engineer hidden profits through tracked parked assets.

Consider a case study: Rohit runs an unregistered cash-heavy business and hasn’t filed his ITR. Over the year, he deploys capital into various assets:

- Stock Market: ₹3 Lakhs

- Gold Purchases: ₹2 Lakhs

- Property Downpayment: ₹25 Lakhs

Even without a declared business ledger, the Income Tax system automatically flags this ₹30 Lakhs capital deployment. Under Section 69 of the Income Tax Act (Unexplained Investments), this parked capital mathematically proves a minimum baseline profit. You cannot hide your earnings if you spend or invest them. If Rohit cannot explain the source of this ₹30 Lakhs, it will be taxed at a punitive flat rate of 60% (plus a 25% surcharge and 4% cess, totaling roughly 78%).

Furthermore, if this forensic tracking reveals that undeclared funds have been parked in offshore accounts or foreign assets, the consequences escalate drastically. Under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, such non-disclosure attracts a flat 30% tax plus a severe 90% penalty—effectively resulting in a 120% liability on the value of the undisclosed foreign asset, alongside potential prosecution.

Your Compliance Action Plan: FY 2025-26 & AY 2026-27

You must organize your financial truth before the system organizes it for you. With the financial year having just closed, filing for FY 2025-26 (Assessment Year 2026-27) is your immediate priority. Follow this three-step blueprint:

- Consolidate Data: Download statements for ALL bank accounts (Savings, Current, and Joint) for the full financial year (1st April 2025 to 31st March 2026). Check your AIS/TIS on the Income Tax portal to see exactly what the government already knows.

- Reconcile Truth: Meticulously separate business inflows from personal outflows. Reconcile this with the data reported in your SFT to determine your mathematically provable net profit.

- Disclose & Protect: Accurately disclose this profit in your ITR for AY 2026-27 before the statutory deadlines (usually July 31st for non-audit cases). Ensure you have verified whether your gross receipts require a GST registration.

Your bank statement is your ultimate reality. Don’t wait for a compliance notice to get your books in order. Take control of your financial footprint today.