Expert Insights from CAshahnawaz.com | Navigating the Income Tax Act 1961 & The Historic 2025 Transition

Welcome to CAshahnawaz.com! If you manage a charitable trust, NGO, educational institution, or Section 8 company in India, staying perfectly compliant with the Income Tax Department’s donation reporting rules is critical to your organization’s survival. This comprehensive, deep-dive guide breaks down everything you need to know about filing your donation statements, maintaining immaculate audit trails, avoiding crippling penalties, and preparing for the monumental legislative shifts coming with the Income Tax Act 2025.

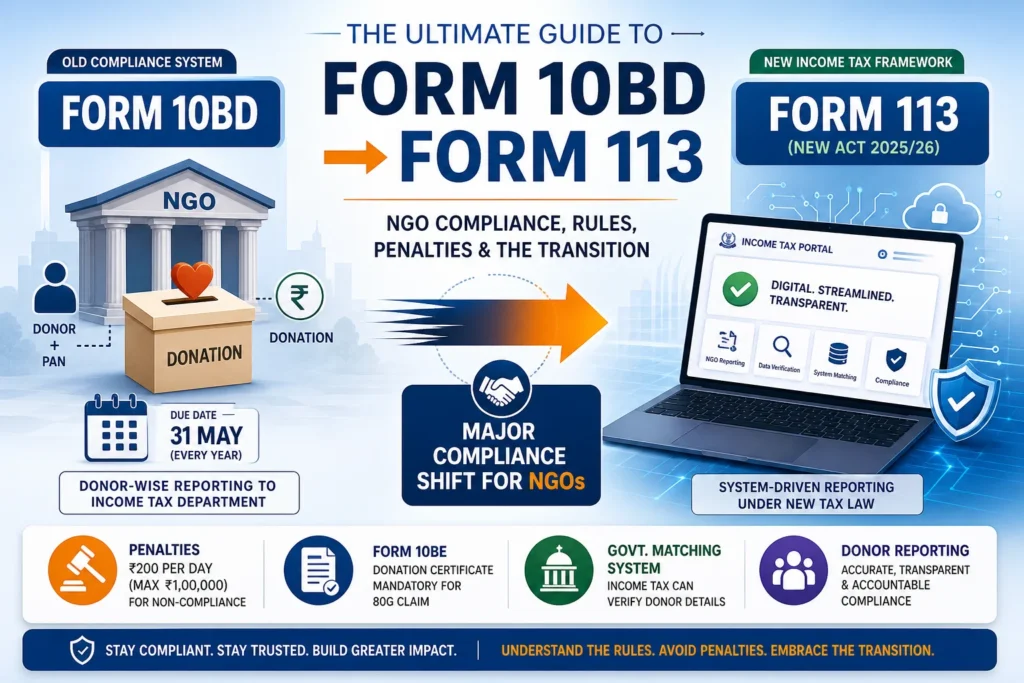

1. The Genesis of Form 10BD: Why Was It Introduced?

Historically, verifying charitable deductions in India was a highly manual, paper-based process that left massive room for information gaps, fabricated receipts, and unverified tax claims. Donors would claim 80G deductions based on physical paper receipts, and the Income Tax Department had no centralized, digital ledger to cross-verify if the NGO actually received those exact funds.

To permanently digitize and secure this ecosystem, the Central Board of Direct Taxes (CBDT) introduced Form 10BD via Notification No. 19/2021. This form acts as a transparent, unbreakable audit trail, effectively functioning for NGOs the same way the TRACES (TDS) system functions for salaried employees. By legally forcing the donee NGO to compile the data, validate the PANs, and upload a master CSV file to a secure sovereign server, the tax credit is automatically populated into the taxpayer’s Annual Information Statement (AIS).

Once you successfully upload the Form 10BD CSV file, the portal automatically generates Form 10BE, which is the official certificate of donation. You must download Form 10BE and issue it to your donors, as it serves as their absolute, sole proof to successfully claim tax deductions while filing their personal Income Tax Returns.

2. Applicability: Who is Legally Obligated to File Form 10BD?

It is a widespread misconception among trust administrators that every registered NGO must file this form. This is incorrect. Form 10BD is strictly mandatory only for entities that hold specific statutory approvals allowing their donors to claim tax benefits.

You must file this form if your organization is approved under:

- Section 80G(5)(viii): This covers the vast majority of charitable institutions, public trusts, and poverty-relief funds.

- Section 35(1A)(i): This covers universities, colleges, or institutions exclusively engaged in scientific research or statistical research.

The 12AB Exemption Caveat: If your trust holds a general tax exemption for its own internal income under Section 12AA or Section 12AB, but does not hold an active 80G or 35(1) approval, you are fundamentally exempt from filing Form 10BD. Since your donors cannot claim tax deductions for their contributions, there is no legal requirement to report their transactions to the portal.

3. Essential Documents and the CSV Data Architecture

To ensure a frictionless upload without facing catastrophic validation errors on the e-filing portal, trusts must maintain exhaustive records year-round. Because major NGOs often process thousands of micro-transactions, manual entry is impossible. The data must be consolidated into a Comma-Separated Values (CSV) file.

- Donor Identification (The Most Critical Metric): You must maintain a robust donor register capturing the name, address, and a Unique Identification Number (UIN) for every single contributor. While the portal technically accepts a Passport, Voter ID, or Driving License, aggressively capturing the donor’s Permanent Account Number (PAN) is strategically paramount. If you upload a donation using a non-PAN identifier, the tax benefit will not automatically reflect in the donor’s AIS.

- Row Limitations: A single CSV file can accommodate a maximum of 25,000 rows. For organizations with massive retail donation models exceeding this limit, the law explicitly permits the filing of multiple Form 10BDs for the same financial year.[1]

- Categorization: Every single donation must be precisely categorized as a Corpus Donation (funds for long-term retention), a Specific Grant (which explicitly includes Corporate Social Responsibility/CSR funds), or an “Others” General Voluntary Contribution (funds meant for general operational deployment).

4. Navigating Edge Cases: The Danger Zone of What NOT to Upload

Administrators must be incredibly careful not to upload certain transactions on Form 10BD. Reporting these incorrectly can trigger severe tax scrutiny or result in invalid certificates being issued to donors.

- Cash Donations Over Rs. 2,000: Under Section 80G(5D), donors cannot claim tax deductions for cash donations that exceed Rs. 2,000. It is an industry best practice to exclude these high-value physical cash donations from Form 10BD. If uploaded, the portal will generate a Form 10BE that explicitly flags the donation as ineligible, which often leads to donor dissatisfaction. Furthermore, accepting cash donations of Rs. 2,00,000 or more from a single person attracts a 100% penalty under Section 269ST.[2]

- Anonymous Donations (The 30% Tax Trap): Donations collected via cash boxes where the donor’s identity and address cannot be verified absolutely cannot be reported on Form 10BD. Under Section 115BBC, if your anonymous donations exceed Rs. 1,00,000 or 5% of your total donations (whichever is higher), that excess amount will be subjected to a punishing 30% penal tax rate.

- Donations in Kind: Contributions of real estate, food, computers, medical equipment, or professional services do not qualify for an 80G monetary tax deduction. These should generally be kept off this specific filing to prevent the automated generation of legally invalid deduction certificates.

5. The Reconciliation Trap: Form 10BD vs. ITR-7

A major area where trusts face scrutiny from Assessing Officers is the mismatch between the macro-financials reported in their annual tax return (ITR-7) and the micro-data uploaded in Form 10BD.

Schedule VC (Voluntary Contributions) of the ITR-7 demands a detailed breakup of all income earned. The aggregate values reported across all filed Form 10BDs should logically align with the gross figures declared in Schedule VC. If your ITR-7 shows Rs. 5 Crores in donations, but your Form 10BD only accounts for Rs. 3 Crores, the tax department may suspect the remaining Rs. 2 Crores are anonymous donations and attempt to tax them heavily under Section 115BBC. Auditing fiduciaries must always maintain a strict internal reconciliation statement explaining any genuine variances (such as large foreign non-PAN grants governed by FCRA).

6. The Punitive Penal Framework: Sections 234G and 271K

The Income Tax Department shows zero leniency for missing the May 31st deadline. Defaulting triggers a dual-penalty mechanism that inflicts financial damage upon the organization while destroying the donor’s tax profile:

- Section 234G Mandatory Late Fees: A strict, non-negotiable late fee of Rs. 200 per day applies for every single day the delay continues beyond the May 31st deadline. However, a legislative safeguard exists: the total quantum of this late fee is legally capped and cannot exceed the total amount of the donation required to be reported.[2]

- Section 271K Discretionary Penalties: Distinct from the daily fee, the Assessing Officer possesses the power to impose a direct, massive penalty ranging from a minimum of Rs. 10,000 up to a maximum of Rs. 1,00,000 for failing to furnish the statement or for failing to issue the generated Form 10BE certificates to your donors.[3]

7. The Future: Preparing for the Income Tax Act 2025 and Form 113

India is currently undergoing a historic tax transformation. The newly enacted Income Tax Act 2025 will entirely replace the legacy 1961 Act, effective April 1, 2026. For NGOs and trust auditors, the philosophy of digital donation tracking remains identical, but the statutory nomenclature and the forms are changing completely.

Visual Evidence from the Portal: The e-Filing interface explicitly outlines the transition. For FY 2025-26, Form 10BD is selected alongside a statutory red warning mandating the shift to Form 113 for Tax Year 2026-27.

As explicitly shown in the official Income Tax portal interface analyzed above, the system is actively preparing for this monumental shift:

- The Interface Warning: When selecting the Financial Year (F.Y) 2025-26, the portal requires the submission of the legacy Form 10BD. However, a prominent red warning has been embedded by the CBDT: “Note: Effective 1st April 2026, donations pertaining to Tax Year 2026-27 and onwards shall be reported using Form 113. Users are required to select this form under the ‘Forms as per Income Tax Act 2025’.”

- The New UI for 2026: Consequently, selecting Tax Year (T.Y) 2026-27 shifts the user to the new interface header: “Statement or Correction Statement to be filed by Donee under section 354(1) [Form No. 113]”.

- Section 80G Becomes Section 354(1): The overarching statutory framework granting tax deductions for philanthropic contributions is transitioning from Section 80G to Section 354(1) of the new 2025 Act.

- Form 114 Replaces Form 10BE: The certificate of donation generated by the portal and issued to your taxpayers will be formally issued as Form 114 starting from Tax Year 2026-27.

8. Comprehensive Dos and Don’ts for NGO Compliance Officers

To successfully navigate this unforgiving regulatory environment and avoid catastrophic CSV validation errors, trust administrators must internalize these rigorous operational protocols:

- Mandate Pre-Transaction PAN Collection: Institutionalize a rigid policy where a donor’s PAN or Aadhaar is collected at the exact point of donation solicitation. Treat identity capture as an absolute prerequisite.

- Pre-Validate PAN Data: Utilize NSDL portals or API integrations to proactively verify donor PANs against the sovereign database prior to compiling your CSV to prevent mass upload failures.

- Utilize Pre-ARNs: Generate the maximum allowable 1,000 Pre-Acknowledgement Numbers at the start of the year. Embed these into your receipting software to create a flawless real-time audit trail.

- Report CSR Grants Correctly: Always include Corporate Social Responsibility (CSR) funds in your filing. Strictly classify them as “Specific Grants,” regardless of whether the corporate entity deducted TDS.

- Ensure Mathematical Symmetry: Before uploading Form 10BD, conduct a macro-level reconciliation to ensure the gross sum of your CSV perfectly mirrors the disclosures made in Schedule VC of your ITR-7.

- File Revised Returns for Errors: If a donor’s PAN is entered incorrectly, immediately file a “Revised” Form 10BD. The system will overwrite the error and generate a corrected Form 10BE certificate.[4]

- Don’t Delay Beyond May 31st: Never defer the filing. A 24-hour delay activates the Rs. 200/day penalty under Section 234G and exposes your trust to the Rs. 1,00,000 penalty under Section 271K.

- Don’t Upload Anonymous Donations: Never attempt to report untraceable physical cash collections or donation box receipts on Form 10BD. Assess them entirely separately to manage the 30% tax risk under Section 115BBC.

- Don’t Include High-Value Cash: Do not report cash donations exceeding Rs. 2,000 with the false expectation that the portal will grant the donor an 80G benefit. Refuse cash donations reaching Rs. 2,00,000 entirely.

- Don’t Report In-Kind Transfers: Exclude property, technology, and food donations from the Form 10BD CSV to prevent the generation of legally invalid monetary deduction certificates.

- Don’t Ignore CSV Formatting: Do not treat numerical fields sloppily. Common errors like treating ZIP codes as numbers (which strips leading zeros) or using inconsistent labels will cause validation failure.

- Don’t File “Nil” Returns: If your organization genuinely received zero eligible donations in the financial year, do not attempt to file a Nil Form 10BD. The portal architecture currently does not accommodate or require it.