01Why Healthcare Demands Special Tax Attention

The healthcare sector in India is one of the most complex verticals from an income tax compliance standpoint. A single practitioner — a doctor running a polyclinic with an attached pharmacy and diagnostic lab — simultaneously straddles professional income rules, GST exemptions and taxable supplies, TDS obligations as both deductor and deductee, and presumptive taxation thresholds.

The arrival of the Income Tax Act, 2025 (effective from AY 2026-27) has reshuffled several section numbers that healthcare professionals had memorised over decades, creating fresh compliance risks for those not updated. Add to this the CBDT's enhanced data-matching capabilities (AIS/26AS/SFT), and healthcare is now one of the most scrutinised sectors by the Income Tax Department.

Shahnawaz and Associates, Chartered Accountants, Mumbai, has prepared this comprehensive guide to address every major compliance question for the healthcare sector — from a solo GP filing ITR-4 to a multi-specialty hospital filing ITR-6.

02Income Tax Act 2025 — Critical Section Changes for Healthcare

The Income Tax Act, 2025 is a structural re-codification. Tax rates, thresholds, and policy intent remain unchanged — only the section numbering and arrangement have been rationalised. For healthcare professionals, the three most disruptive migrations are highlighted below.

Complete Cross-Reference Table — Healthcare-Relevant Sections

| Topic | Old Section (IT Act 1961) | New Section (IT Act 2025) | Healthcare Relevance |

|---|---|---|---|

| Presumptive Tax — Professionals | Sec 44ADA | Sec 46 / Sec 58 | Doctors, physiotherapists, vets with receipts ≤ ₹75L |

| Presumptive Tax — Business | Sec 44AD | Sec 46 / Sec 58 | Pharmacy, medical store (non-professional entity) |

| Tax Audit trigger | Sec 44AB | Sec 44 / Sec 63 | Hospitals exceeding ₹1Cr (business) or ₹75L (professional) |

| Books of Accounts | Sec 44AA | Sec 62 | Mandatory for doctors with professional receipts > ₹1.5L |

| MSME payment disallowance | Sec 43B(h) | Sec 37(2)(g) | Hospitals paying medical suppliers who are MSMEs |

| Depreciation on equipment | Sec 32 | Sec 33 | MRI, CT scan, X-ray, surgical instruments |

| Business income incl. perquisites | Sec 28(iv) | Sec 26(iv) | Pharma gifts, sponsored conferences, demo kits |

| Deductions for business expenses | Sec 37(1) | Sec 33 | Professional expenses, repairs, consumables |

| 80C / NPS deductions | Chapter VI-A | Sec 123–132 | Doctors claiming PPF / NPS / health insurance |

| Carry forward of losses | Sec 72 | Sec 97 | New hospitals with losses in early years |

03Entities & Business Sub-Types Covered

Each of these sub-types has different ITR form obligations, GST registration requirements, presumptive taxation eligibility, and books of accounts requirements. A single doctor in solo practice has radically different compliance obligations than a multi-entity hospital group — and this guide addresses both ends of the spectrum and everything in between.

04Which ITR Form to Use — Healthcare Decision Framework

Choosing the wrong ITR form renders the return defective and may trigger a Sec 139(9) defective return notice. The form selection hinges on entity type, income classification, and whether presumptive taxation applies.

05Presumptive Taxation for Doctors — Section 46 (formerly Sec 44ADA)

The presumptive taxation scheme under Section 46 / Section 58 of the Income Tax Act 2025 (formerly Section 44ADA of the 1961 Act) is the single most important provision for individual medical practitioners in India. When applicable, it eliminates the need for maintaining detailed books of accounts and allows 50% of gross receipts to be declared as taxable profit — with no questions asked on the remaining 50%.

| Parameter | Details |

|---|---|

| Eligible Assessees | Individuals and HUFs who are medical professionals (MBBS, MD, MS, Dental, Veterinary, etc.) |

| Gross Receipts Limit | ≤ ₹75 Lakhs in the previous year (AY 2026-27) |

| Deemed Profit | Minimum 50% of gross receipts must be declared as income |

| Opt-Out Consequence | If profit declared is below 50%, full books + tax audit mandatory for next 5 years |

| Books of Accounts | Not required if opting for presumptive — exempt under Sec 62 (old 44AA) |

| Entities Excluded | Companies, LLPs, firms — presumptive available only to individuals/HUF |

Step-by-Step: Applying the Presumptive Scheme

06Tax Audit — Section 44 / Section 63 (formerly Section 44AB)

Under the Income Tax Act 2025, Section 44 and Section 63 replicate the tax audit framework previously under Sec 44AB of the 1961 Act. The audit report must be obtained from a practicing Chartered Accountant and submitted before the ITR filing due date.

| Entity Type | Threshold for Tax Audit (AY 2026-27) | Audit Report Form | Due Date |

|---|---|---|---|

| Individual Doctor (Professional) | Gross Receipts > ₹75 Lakhs | Form 3CB + 3CD | 30 September 2026 |

| Doctor opting out of Presumptive | Any receipts (if declaring <50%) | Form 3CB + 3CD | 30 September 2026 |

| Pharmacy / Medical Store (Business) | Turnover > ₹1 Cr (cash), ₹10 Cr (95%+ digital) | Form 3CB + 3CD | 30 September 2026 |

| Hospital / Nursing Home (Company) | As per company law thresholds | Form 3CA + 3CD | 30 September 2026 |

| Charitable Hospital Trust | Total income > ₹2.5 Crore (approx) | Form 10B + 3CA/3CB | 30 September 2026 |

Key Form 3CD Clauses Specific to Healthcare

- Clause 19 — Amounts debited for personal expenses (doctors routing personal expenses through clinic books)

- Clause 21 — Inadmissible deductions including any expenses violating CBDT's pharma gift circular

- Clause 26 — MSME payment compliance (Sec 37(2)(g) / old Sec 43B(h))

- Clause 30 — Details of loans/deposits taken or repaid in cash exceeding ₹20,000 — important for cash-heavy OPDs

- Clause 44 — Breakup of expenditure into GST registered/unregistered suppliers — critical for hospitals with high procurement volumes

07Books of Accounts — Section 62 (formerly Section 44AA)

Under Section 62 of the Income Tax Act 2025 (successor to Sec 44AA of the 1961 Act), medical professionals are specifically listed among categories required to maintain prescribed books of accounts when income exceeds ₹1,50,000 or gross receipts exceed ₹25 Lakhs in any of the 3 immediately preceding years.

| Register / Record | Content Required | Purpose in Scrutiny |

|---|---|---|

| Patient Register / OPD Register | Patient name, date, fees charged, mode of payment | Primary income evidence — absence is fatal in scrutiny |

| Fee Collection Register | Daily fee receipts, cash vs digital breakup | Reconcile with bank deposits; identify cash receipts > ₹2L |

| Surgical / Procedure Register | Type of procedure, surgeon, fees, IPD reference | Verify high-value surgical income claims |

| Drug / Dispensing Register | Medicines prescribed/dispensed, quantity, source | Reconcile pharmacy purchase vs dispensing |

| Lab Test Register | Tests performed, charges, referring doctor | Verify lab income; cross-check with reagent purchase |

| Staff Salary Register | Name, designation, monthly salary, TDS details | Verify salary deduction claims; TDS compliance |

| Equipment Depreciation Schedule | Asset name, date of purchase, cost, WDV, rate | Verify depreciation claims on MRI, X-Ray, surgical instruments |

| Cash Book & Bank Book | Daily receipts and payments | Primary accounting record; auditor's starting point |

08GST in Healthcare — Exemptions, Taxable Supplies & Practical Issues

GST in healthcare is a maze of exemptions and taxable supplies that can exist under the same roof. A hospital simultaneously provides GST-exempt medical services and taxable pharmacy supplies. Getting this wrong has dual consequences — GST liability/penalties and income tax implications (incorrect ITC claims).

| Supply Type | GST Rate | SAC/HSN | Key Condition / Note |

|---|---|---|---|

| Medical consultation fees | EXEMPT | 9993 | Services by authorised medical practitioners |

| In-patient / IPD hospital services | EXEMPT | 9993 | Including nursing, surgical, diagnostic as composite supply |

| Diagnostic tests (labs) | EXEMPT | 9993 | Blood test, X-ray, MRI when by authorized medical entity |

| Ambulance services | EXEMPT | 9993 | All operators including private ambulances |

| Veterinary clinic services | EXEMPT | 9993 | Animal care services by veterinary doctors |

| Medicines (essential / life-saving drugs) | NIL to 5% | 3004 | Life-saving drugs typically NIL; others 5% |

| Medicines (general OTC) | 12% | 3004 | Typical pharmacy retail — 12% GST |

| Medical devices (basic) | 5%–12% | 9018–9022 | Stents, prosthetics lower rated; complex devices 12% |

| Cosmetic surgery (non-medically necessary) | 18% | 9993 | Not a "healthcare" service — fully taxable |

| Hair transplant / aesthetic procedures | 18% | 9993 | CBIC clarification — cosmetic, not medical |

| Wellness / Gym packages at hospital | 18% | 9995 | Wellness services by hospitals — fully taxable |

| Rent of medical equipment to others | 18% | 9973 | Leasing MRI/equipment — taxable rental supply |

09TDS Obligations in Healthcare

As a TDS Deductor (Hospital / Nursing Home / Clinic)

| Payment Type | New TDS Section 393(1) Code | Old Sec | Rate | Threshold |

|---|---|---|---|---|

| Visiting / Consultant Doctors/ Professional Services (Legal, Advocate, counselor) | 1027 | 194J | 10% | > ₹50,000single / ₹1L aggregate. |

| Staff Salaries | Sec 392 | 192 | Slab rate | Above basic exemption |

| Rent (building/equipment) | 1008/1009 | 194I | 2% (P&M), 10% (land/building) | > ₹50,000/-pm |

| Housekeeping / Laundry Contracts/Medical Equipment Maintenance/ Catering/ Food contract | 1024 | 194C | 1% (individual), 2% (company) | > ₹30,000 single / ₹1L aggregate |

10Pharma Company Gifts & Conferences — A Taxable Trap

This is one of the most consistently litigated issues in healthcare taxation. CBDT Circular No. 5 of 2012 clarifies that gifts, hospitality, travel, and conference expenses given by pharmaceutical companies to doctors are taxable in the hands of the receiving doctor.

From the doctor's side: The benefit received is taxable as a perquisite / benefit in profession under Sec 26(iv) of the 2025 Act (old Sec 28(iv)). Foreign trips, luxury hotel stays, expensive medical equipment gifts from pharma companies must all be reported in the ITR.

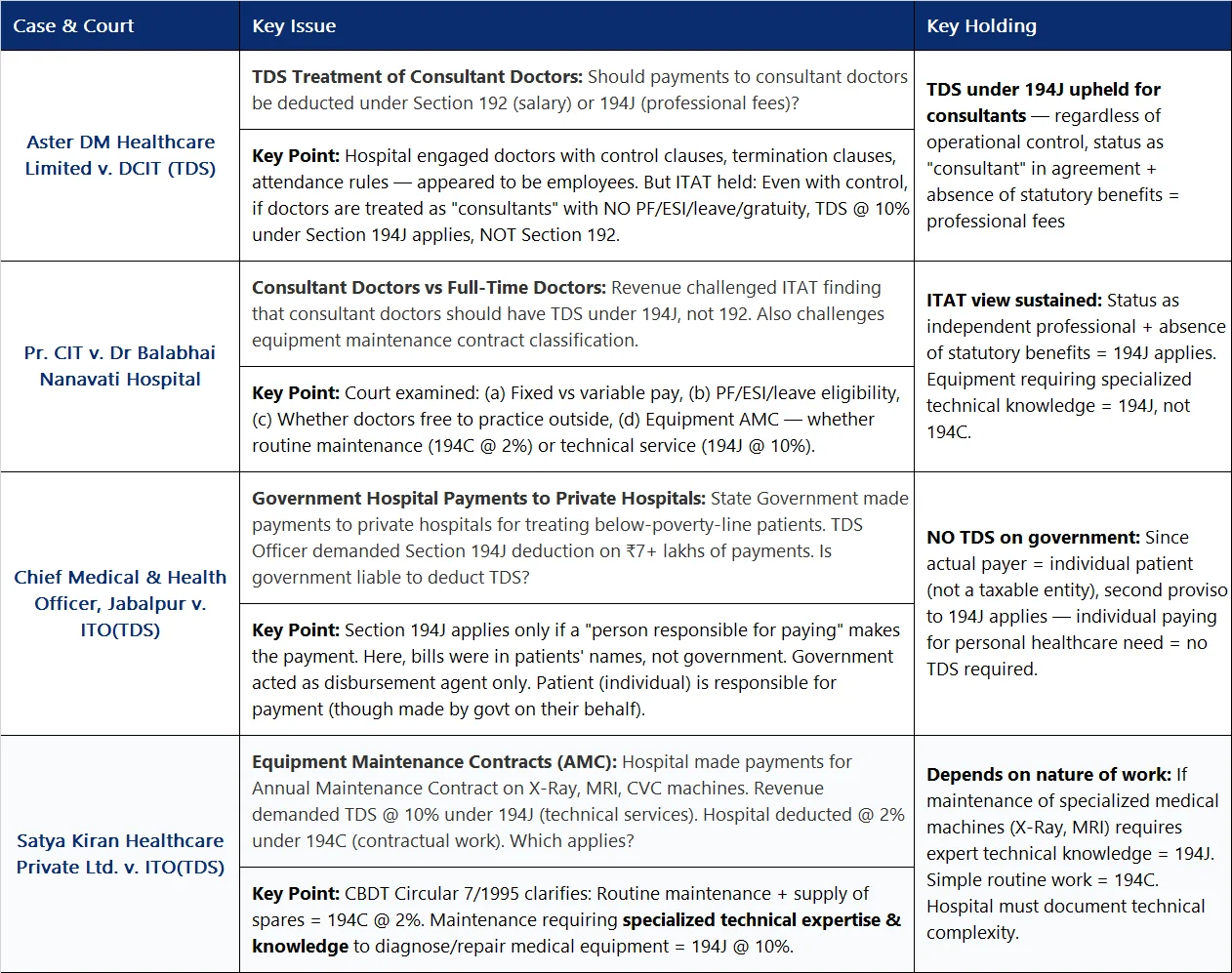

11Important Case Laws — Healthcare & Income Tax

12MSME Payment Compliance — Section 37(2)(g) (formerly Section 43B(h))

Effective from AY 2024-25 onwards (continuing under IT Act 2025), any amount payable to a Micro or Small Enterprise (as per the MSMED Act, 2006) must be paid within the stipulated time to be deductible in the year of accrual.

If there is NO written agreement: payment must be made within 15 days of delivery.

If payment is not made within this period, the expense is disallowed in the year of accrual and is only deductible in the year of actual payment.

Hospitals and nursing homes typically procure from many MSME vendors — medical consumables suppliers, surgical glove manufacturers, linen suppliers, biomedical waste management companies, and diagnostic reagent vendors are frequently MSMEs. A hospital with ₹5 crore of annual MSME procurement and typical 60-90 day payment cycles could face ₹50-80 lakh of disallowance under this provision.

Action required: Request Udyam Registration certificates from all suppliers, tag MSME status in your vendor master, identify outstanding payables to MSMEs as at 31st March beyond the permitted period, add them back in tax computation, and disclose in Form 3CD Clause 26.

13Depreciation on Medical Equipment — Section 33 (formerly Section 32)

For hospitals and large clinics, depreciation is often the single largest deduction. Getting the depreciation rates, block classification, and timing of capitalisation right is essential.

| Asset Category | Depr Rate | Block | Note |

|---|---|---|---|

| Hospital Building (owned) | 10% | Buildings | Separate block if exclusively for medical use |

| MRI Machine, CT Scanner | 15% | Plant & Machinery | Standard P&M rate |

| X-Ray, ECG, EEG, Ultrasound Units | 15% | Plant & Machinery | Standard P&M rate |

| Computers & Diagnostic Software | 40% | Computers | Hospital management software, imaging software |

| Surgical Instruments (Reusable) | 15% | Plant & Machinery | Laparoscopic equipment, surgical tools |

| Oxygen Plants, Ventilators, ICU equipment | 15% | Plant & Machinery | Life support equipment |

| Ambulance Vehicles | 15% | Motor Vehicles | Standard motor vehicle rate |

| Furniture — Hospital Beds, Stretchers | 10% | Furniture | Includes OT tables, ward beds |

| Solar Panels (Hospital Energy) | 40% | Plant & Machinery | Accelerated depreciation for renewable energy |

14Key Deductions Available to Healthcare Professionals

| Deduction | New Act Section | Old Act Section | Max Amount | Healthcare Relevance |

|---|---|---|---|---|

| LIC / PPF / ELSS / Home Loan Principal | Sec 123 | 80C | ₹1,50,000 | Doctor's personal tax planning |

| NPS (Employee contribution) | Sec 124 | 80CCD(1) | ₹50,000 additional | Doctors enrolled in NPS |

| Health Insurance Premium | Sec 126 | 80D | ₹25,000–75,000 | Self + parents (senior citizen) |

| Preventive Health Check-up | Sec 126 | 80D | ₹5,000 | Within 80D limit |

| Donations to 80G trusts | Sec 132 | 80G | 50–100% of donation | Donations to charitable hospital / PM CARES |

| Interest on housing loan | Sec 89 | 24(b) | ₹2,00,000 | Doctor's self-occupied property |

15Practical Do's & Don'ts — Healthcare ITR Filing AY 2026-27

- ✅ Reconcile AIS + 26AS with every bank account before filing — check TDS entries from all hospitals you consult at

- ✅ Maintain OPD register with clear fee and payment-mode columns; mark nil-fee consultations contemporaneously

- ✅ Segregate pharmacy income from professional income — different GST treatment, different ITR schedules

- ✅ Claim depreciation on all equipment under Sec 33 (old Sec 32) using correct rates

- ✅ Disclose pharma company benefits (trips, gifts, demo kits) under Sec 26(iv)

- ✅ Collect Udyam Registration from medical suppliers; pay MSMEs within 45 days

- ✅ File ITR before 31 July (no audit) or 30 September (tax audit applicable)

- ✅ Use ITR-3 if gross receipts exceed ₹75L or you have capital gains

- ✅ Pay advance tax in single instalment by 15th March (presumptive tax filers)

- ✅ Disclose foreign assets and foreign conference travel in Schedule FA / FSI

- ❌ Don't understate gross receipts to stay within ₹75L presumptive limit — AIS now captures UPI, digital, and insurance TPA payouts

- ❌ Don't treat visiting consultant income as non-reportable — TDS in 26AS will reflect it even if you don't disclose

- ❌ Don't mix pharmacy (business) and clinical (professional) cash flows in a single bank account

- ❌ Don't accept cash receipts above ₹2 lakh from a single patient — Sec 269ST attracts 100% penalty equal to amount received

- ❌ Don't claim ITC on inputs used exclusively for exempt healthcare services

- ❌ Don't omit TDS on visiting consultant payments — even a single payment > ₹30,000 triggers 194J obligation

- ❌ Don't route personal expenses (school fees, home renovation, family holidays) through clinic books

- ❌ Don't forget Form 10-IE (new tax regime opt-in) if switching regime for business/professional income

- ❌ Don't ignore advance tax — default on Sec 234B/234C interest can be ₹10,000–₹1 lakh+ for high-earning specialists

- ❌ Don't reference old section numbers (44ADA, 44AB, 43B(h)) in documents — use IT Act 2025 numbers

16Special Topics — Charitable Hospitals, NRI Doctors & Tax Regime

Charitable Hospitals (Section 12AB Registration)

Hospitals and dispensaries registered as charitable trusts or Section 8 companies can claim exemption under Sec 11/12 equivalent of the IT Act 2025 provided: (a) at least 85% of income is applied for charitable purposes in the same year; (b) surplus is accumulated for up to 5 years for specific projects; and (c) the hospital must not benefit any specific religious community for the "secular" exemption to apply. Post-2022 amendments, all charitable hospitals must have both Sec 12AB registration and Sec 80G approval to receive tax-exempt donations.

NRI / Returning Doctor — Tax Issues

Doctors who practiced abroad and have returned to India, or who split the year between India and abroad, face complex residency + DTAA issues. If a doctor practices in India for more than 182 days in a previous year, they are ordinarily resident and their global income is taxable in India. Income from foreign hospitals/telemedicine platforms must be disclosed under Schedule FSI. Applicable DTAA (with UK, US, UAE, Singapore, Australia) may provide relief — but DTAA relief requires Form 67 filing and foreign tax credit claims.

Old vs New Tax Regime — Which Works for Doctors?

The new tax regime (now the default regime under the Income Tax Act 2025) offers lower slab rates but eliminates most deductions (80C equivalent, HRA, professional deductions under old scheme). For doctors with high professional expenses, large depreciation claims, and significant 80C/NPS contributions, the old regime typically yields lower tax. For young doctors with minimal investments and high income, the new regime may be beneficial. Always run the computation both ways — Shahnawaz and Associates provides a regime comparison as part of our filing service.

17Healthcare Compliance Calendar — AY 2026-27 Key Dates

| Due Date | Compliance | Who |

|---|---|---|

| 15 June 2026 | Advance Tax — 1st instalment (15% of annual liability) | All doctors/hospitals with tax > ₹10,000 |

| 31 July 2026 | ITR Filing — non-audit cases | Doctors under Sec 46 presumptive; individual doctors with no audit |

| 15 September 2026 | Advance Tax — 2nd instalment (45% cumulative) | All healthcare entities with advance tax obligation |

| 30 September 2026 | Tax Audit Report (Form 3CA/3CB + 3CD) | Hospitals, clinics, labs above audit threshold |

| 31 October 2026 | ITR Filing — audit cases | Hospitals, nursing homes, corporate health entities |

| 15 December 2026 | Advance Tax — 3rd instalment (75% cumulative) | All taxpayers except presumptive |

| 15 March 2027 | Advance Tax — 4th instalment (100%); Single instalment for presumptive taxpayers | All healthcare taxpayers |

| 7th each month | TDS deposit for deductions in previous month | All hospitals/clinics deducting TDS on salaries, 194J, 194C, 194I |

| 20th each month | GSTR-3B filing | Pharmacy, cosmetic surgery clinics, GST registered healthcare entities |

18Common Scrutiny Triggers — What Gets Healthcare ITRs Noticed

The CASS (Computer Assisted Scrutiny Selection) system has specific filters for the healthcare sector. Understanding these helps file more carefully and maintain better documentation.

- 🔴 Large cash deposits in bank accounts not matching disclosed professional income — AIS captures every bank's cash deposit data via SFT

- 🔴 High lifestyle expenses vs. declared income — foreign travel, luxury vehicle registration, property registration data cross-matched via Annual Information Statement

- 🔴 Significant unexplained year-on-year income drop — post-COVID, the department expects recovery; unexplained drops are red-flagged

- 🔴 TDS in 26AS showing income not disclosed in ITR — TDS under 194J appearing but no professional income declared

- 🔴 Insurance TPA payments — health insurance companies file SFT on payments to hospitals; TPA receipts must match ITR

- 🔴 GST turnover vs. ITR income mismatch — if GSTR-1 shows ₹40L but ITR declares ₹25L, automated scrutiny is automatic

- 🔴 Multiple bank accounts with one account not shown in ITR — the department pulls all bank data using PAN linkage

- 🔴 Foreign remittances / SWIFT — any doctor receiving fees from abroad that are not disclosed in Schedule FSI

19Conclusion — File Right, Sleep Well

The healthcare sector's unique combination of exempt and taxable income streams, the professional vs. business income debate, the pharma gift exposure, and the significant section number changes under the Income Tax Act 2025 together create a compliance landscape that demands year-round record-keeping, proactive planning, and expert professional guidance.

The key principles that protect healthcare professionals in any scrutiny: contemporaneous records (OPD registers, fee receipts maintained at the time of the event — not retrospectively); clean accounts (pharmacy separate from clinical, personal separate from professional); honest disclosures (AIS has made hiding income structurally difficult); and correct section references under the new 2025 Act.

At Shahnawaz and Associates, Chartered Accountants, Mumbai, we have been filing ITRs for doctors, hospitals, nursing homes, diagnostic labs, and all allied healthcare entities for years. Our understanding of healthcare-specific tax issues means you get a filing that is technically correct, optimised for your specific entity type, and defensible under scrutiny.

🏥 Need Expert Help with Healthcare ITR Filing?

Shahnawaz and Associates, Chartered Accountants, Jogeshwari West, Mumbai — specialising in ITR filing, Tax Audit, GST compliance, and advisory for doctors, hospitals, clinics and all healthcare entities across India.

Schedule a Free Enquiry 📞 +91 98192 67015