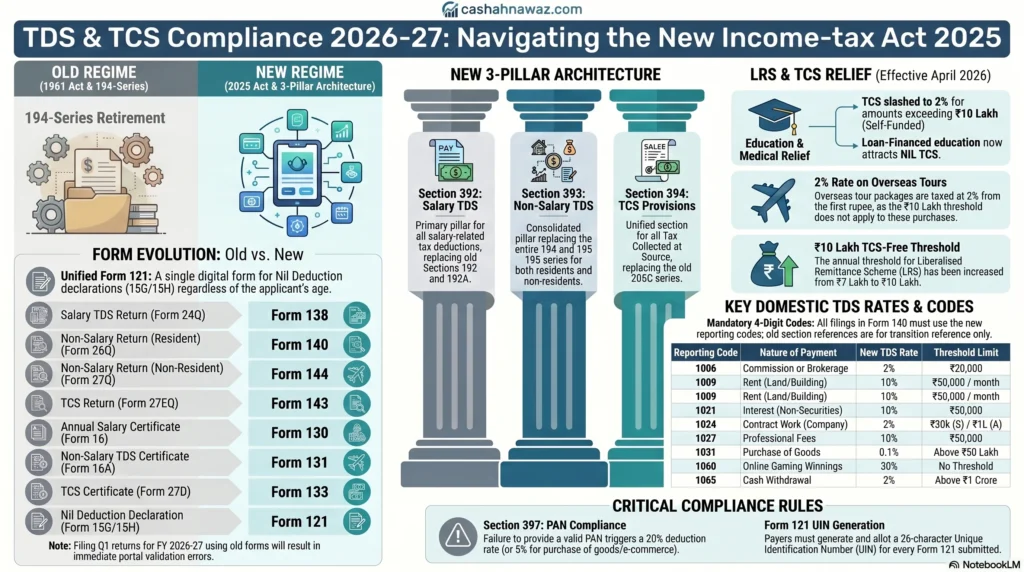

The tax landscape in India has officially transformed. With the Income-tax Act, 2025 coming into full effect from April 1, 2026, the traditional way of filing TDS and TCS returns is obsolete. The old alphabet-soup of sections (194C, 194J, 206C) has been replaced by three master sections, universal reporting codes, and entirely new tax forms.

Furthermore, the recent Budget 2026 has introduced major rate cuts and threshold hikes for foreign remittances. If you are a business owner, deductor, or tax professional, here is your definitive May 2026 guide to staying compliant.

1. The New 3-Pillar Architecture

The Income Tax Act, 2025 has consolidated all TDS and TCS provisions into three main parent sections:

Section 392: Covers all Salary-related TDS (replaces old Sec 192 & 192A).

Section 393: Covers all Non-Salary TDS for both residents and non-residents (replaces the entire 194 and 195 series).

Section 394: Covers all Tax Collected at Source (TCS) provisions (replaces the 206C series).

2. Say Goodbye to Old Forms: The New Form Ecosystem

You can no longer file returns or issue certificates using the old form numbers. Attempting to file Q1 returns for FY 2026-27 using old forms will result in portal validation errors.

| Purpose | Old Form | New Form (FY 2026-27 onwards) |

| Salary TDS Return | Form 24Q | Form 138 |

| Non-Salary TDS Return (Resident) | Form 26Q | Form 140 |

| Non-Salary TDS Return (Non-Resident) | Form 27Q | Form 144 |

| TCS Return | Form 27EQ | Form 143 |

| Annual Salary Certificate | Form 16 | Form 130 |

| Non-Salary TDS Certificate | Form 16A | Form 131 |

| TCS Certificate | Form 27D | Form 133 |

| Nil Deduction Declaration | Form 15G / 15H | Form 121 (Unified digital form for all ages) |

3. Major Relief in LRS & TCS Rules (Effective April 2026)

Budget 2026 brought significant changes to outward foreign remittances under the Liberalised Remittance Scheme (LRS), offering massive relief to students and travelers.

Higher Threshold: The TCS-free threshold has been increased from ₹7 Lakh to ₹10 Lakh per financial year.

Education (Self-Funded) & Medical: TCS slashed to just 2% on amounts exceeding ₹10 Lakh.

Education (Loan-Financed): NIL TCS, regardless of the amount, if funded by a recognized financial institution.

Overseas Tour Packages: TCS slashed to 2% on the full amount (the ₹10 lakh threshold does not apply to tour packages; it is taxed from the first rupee).

Other Purposes (Gifts, Investments): 5% TCS on amounts exceeding ₹10 Lakh (increases to 10% if PAN is not provided).

4. Domestic TDS Rate Chart & Codes (FY 2026-27)

You must use the 4-digit codes in Form 140. The old sections are provided below purely for your reference.

| Reporting Code | Old Section | Nature of Payment | New Section Reference | TDS Rate | Threshold Limit |

| 1005 | 194D | Insurance Commission | 393(1) | 2% (Ind) / 10% (Others) | ₹20,000 |

| 1006 | 194H | Commission or Brokerage | 393(1) | 2% | ₹20,000 |

| 1008 | 194I(a) | Rent on Plant & Machinery | 393(1) | 2% | ₹50,000 / month |

| 1009 | 194I(b) | Rent on Land/Building/Furniture | 393(1) | 10% | ₹50,000 / month |

| 1019 | 193 | Interest on Securities | 393(1) | 10% | ₹10,000 |

| 1021 | 194A | Interest (Other than Securities) | 393(1) | 10% | ₹50,000 |

| 1023 | 194C | Contract Work (Individual/HUF) | 393(1) | 1% | ₹30k (Single) / ₹1L (Agg) |

| 1024 | 194C | Contract Work (Others) | 393(1) | 2% | ₹30k (Single) / ₹1L (Agg) |

| 1026 | 194J(a) | Fees for Technical Services (FTS) | 393(1) | 2% | ₹50,000 |

| 1027 | 194J(b) | Professional Fees | 393(1) | 10% | ₹50,000 |

| 1029 | 194 | Dividend Payments | 393(1) | 10% | ₹10,000 |

| 1031 | 194Q | Purchase of Goods | 393(1) | 0.1% | Above ₹50 Lakh |

| 1035 | 194O | E-commerce Participant Sale | 393(1) | 0.1% | ₹5 Lakh |

| 1067 | 194T | Payments to Partners (Salary/Int) | 393(3) | 10% | ₹20,000 |

Winnings & Cash Withdrawals

| Reporting Code | Nature of Payment | New Section Reference | TDS Rate | Threshold Limit |

| 1058 | Lottery, Crossword, Gambling | 393(3) | 30% | ₹10,000 |

| 1060 | Online Gaming Winnings | 393(3) | 30% | No Threshold |

| 1065 | Cash Withdrawal (Non-Coop Soc) | 393(3) | 2% | Above ₹1 Crore |

Important Compliance Rules for FY 2026-27

Strict PAN Compliance (Section 397): If a deductee does not furnish a valid PAN, tax must be deducted at 20% (or the rate in force, whichever is higher). The exception is for purchase of goods (Code 1031) or e-commerce (Code 1035), where the non-PAN rate is 5%.

Form 121 UIN Processing: When an individual or entity submits the new unified Form 121 for nil deduction, the payer entity must generate and allot a 26-character Unique Identification Number (UIN) to the form.

Binding Circulars: The CBDT has clarified that recent circulars regarding perquisites (Code 1033) and virtual digital assets/crypto (Code 1037/1038) carry mandatory compliance weight.

Disclaimer: Tax laws are dynamic. This update is based on the Income-tax Act, 2025 and CBDT circulars available as of May 2026. For precise tax planning, software updates, or filing assistance, consult our team at cashahnawaz.com